Decline in interest rates on deposits with an agreed maturity

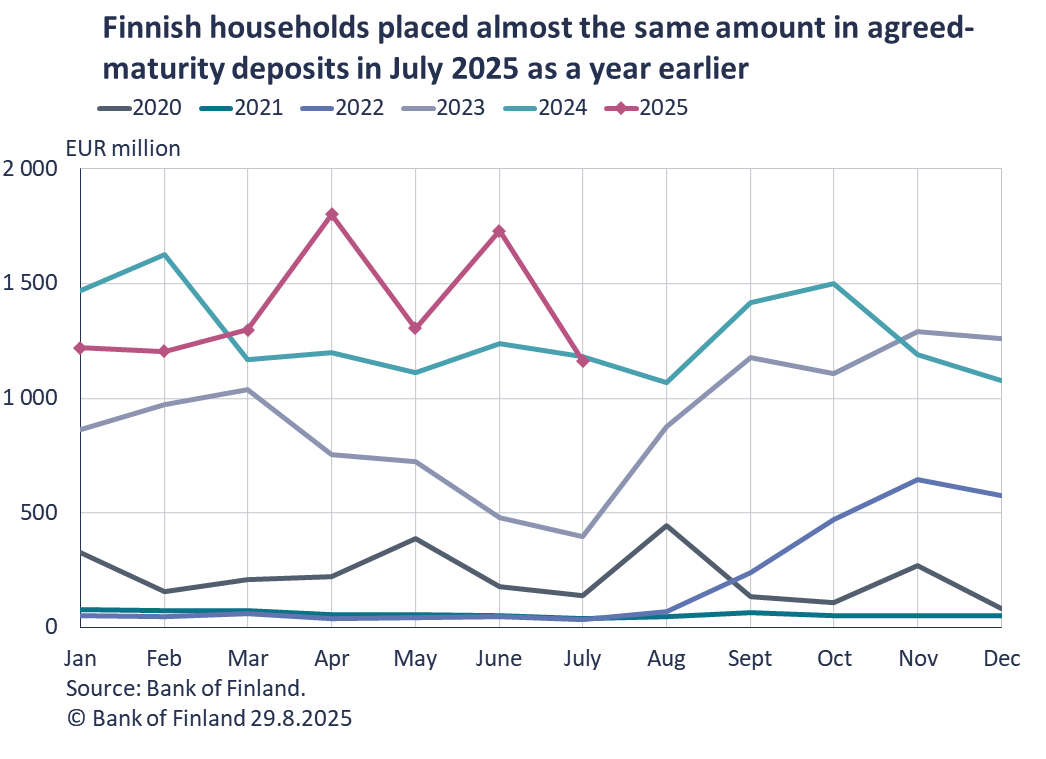

Despite the fall in interest rates, in July 2025 households concluded new agreements on deposits with an agreed maturity almost the same as in July a year earlier. Compared with the average interest rate on overnight deposits (incl. transaction accounts), the interest paid on deposits with an agreed maturity was higher in July.

Despite the fall in interest rates, in July 2025 households concluded new agreements on deposits with an agreed maturity[1] to a value of EUR 1.2 billion, almost the same as in July a year earlier. The average interest rate on these new deposits was 2.10%, down 1.4 percentage points from July 2024. The average interest rate on the total stock of deposits with an agreed maturity was slightly higher, standing at 2.2% in July 2025.

Compared with the average interest rate on overnight deposits[2] (incl. transaction accounts), the interest paid on deposits with an agreed maturity was 1.9 percentage points higher in July. At the end of July 2025, the average interest on the stock of households’ overnight deposits was 0.36%. Correspondingly, the average interest on the stock of households’ investment deposits[3] was 1.2%. At the end of July, the average interest on the aggregate stock of households’ deposits was 0.83%.

At the end of July 2025, Finnish households’ aggregate deposit stock stood at EUR 114.7 billion, and its annual rate of change was 4.3%. Overnight deposits accounted for EUR 69.6 billion of the deposit stock, deposits with an agreed maturity for EUR 15.5 billion and investment deposits for EUR 29.5 billion. The annual rate of change of the overnight deposit stock was 4.4% in July. For the stock of agreed-maturity deposits, the corresponding figure was 8.0% and for the investment deposit stock 2.2%.

Loans

Finnish households drew down new housing loans in July 2025 to a total of EUR 1.3 billion, an increase of EUR 220 million on the same month a year earlier. Buy-to-let mortgages accounted for EUR 120 million of the new drawdowns. The average interest rate on new housing loans rose from June, to 2.74%. At the end of July 2025, the stock of housing loans stood at EUR 105.7 billion, and the annual growth rate of the loan stock was -0.1%. Of the housing loan stock, buy-to-let mortgages accounted for EUR 9.0 billion. At the end of July, Finnish households held EUR 17.6 billion in consumer credit and EUR 17.7 billion of other loans.

Drawdowns of new loans by Finnish non-financial corporations in July totalled EUR 2.1 billion, of which loans to housing corporations accounted for EUR 620 million. The average interest rate on the new drawdowns rose from June and was 3.78%. At the end of July, the stock of loans granted to Finnish non-financial corporations stood at EUR 107.5 billion, of which loans to housing corporations amounted to EUR 45.4 billion.

Loans and deposits to Finland, preliminary data |

|||||

| May, EUR million | June, EUR million | July, EUR million | July, 12-month change1, % | Average interest rate, % | |

| Loans to households, stock | 140,868 | 140,912 | 140,946 | -0.1 | 3.47 |

| - of which housing loans | 105,673 | 105,689 | 105,698 | -0.1 | 2.91 |

| - of which buy-to-let mortgages | 8,922 | 8,932 | 8,951 | 3.02 | |

| Loans to non-financial corporations2, stock | 107,730 | 107,858 | 107,532 | 0.5 | 3.36 |

| Deposits by households, stock | 113,972 | 114,737 | 114,681 | 4.3 | 0.83 |

| Households' new drawdowns of housing loans | 1,273 | 1,377 | 1,270 | 2.74 | |

| - of which buy-to-let mortgages | 110 | 125 | 119 | 2.86 | |

* Includes loans and deposits in all currencies to residents in Finland. The statistical releases of the Bank of Finland up to January 2021, as well as those of the ECB, present loans and deposits in euro to euro area residents and also include non-profit institutions serving households. For these reasons, the figures in this table differ from those in the aforementioned releases.

1 Rate of change has been calculated from monthly differences in levels adjusted for classification and other revaluation changes.

2 Non-financial corporations also include housing corporations.

- Euro-denominated deposits and loans of euro area residents: stock, 12 month rate of change and average interest rate

- Euro-denominated loans and deposits of Finnish households

- New business on loans and new drawdowns of household loans

- Finnish contribution to the euro area monetary aggregates and their main counterparts

- Imputed interest rate margins on loans from MFIs

The next news release on money and banking statistics will be published at 10:00 on 26 September 2025.

[1] Deposits with an agreed maturity include savings deposits for first-home purchase (ASP deposits).

[2] Overnight deposits include transaction accounts and other types of accounts from which funds may be withdrawn or transferred freely.

[3] Investment deposits are deposits redeemable at notice. They do not have a fixed maturity date (unlike deposits with an agreed maturity) but have a notice period during which the deposit cannot be converted into cash without a penalty (unlike overnight deposits). This category also includes investment accounts which do not have a period of notice or agreed maturity but which contain restrictive drawing provisions.