With the rise in interest rates, the popularity of deposits with agreed maturity and of investment deposits[1] has increased among Finnish households, while the popularity of overnight deposits[2] has decreased. In January–September 2023, the share of agreed maturity deposits and investment deposits in households’ total deposits has increased by almost 7 percentage points, as households have moved almost EUR 7 billion of financial assets to deposit accounts with higher interest rates. In the same period, assets held in overnight deposit accounts have contracted by EUR 8.5 billion.

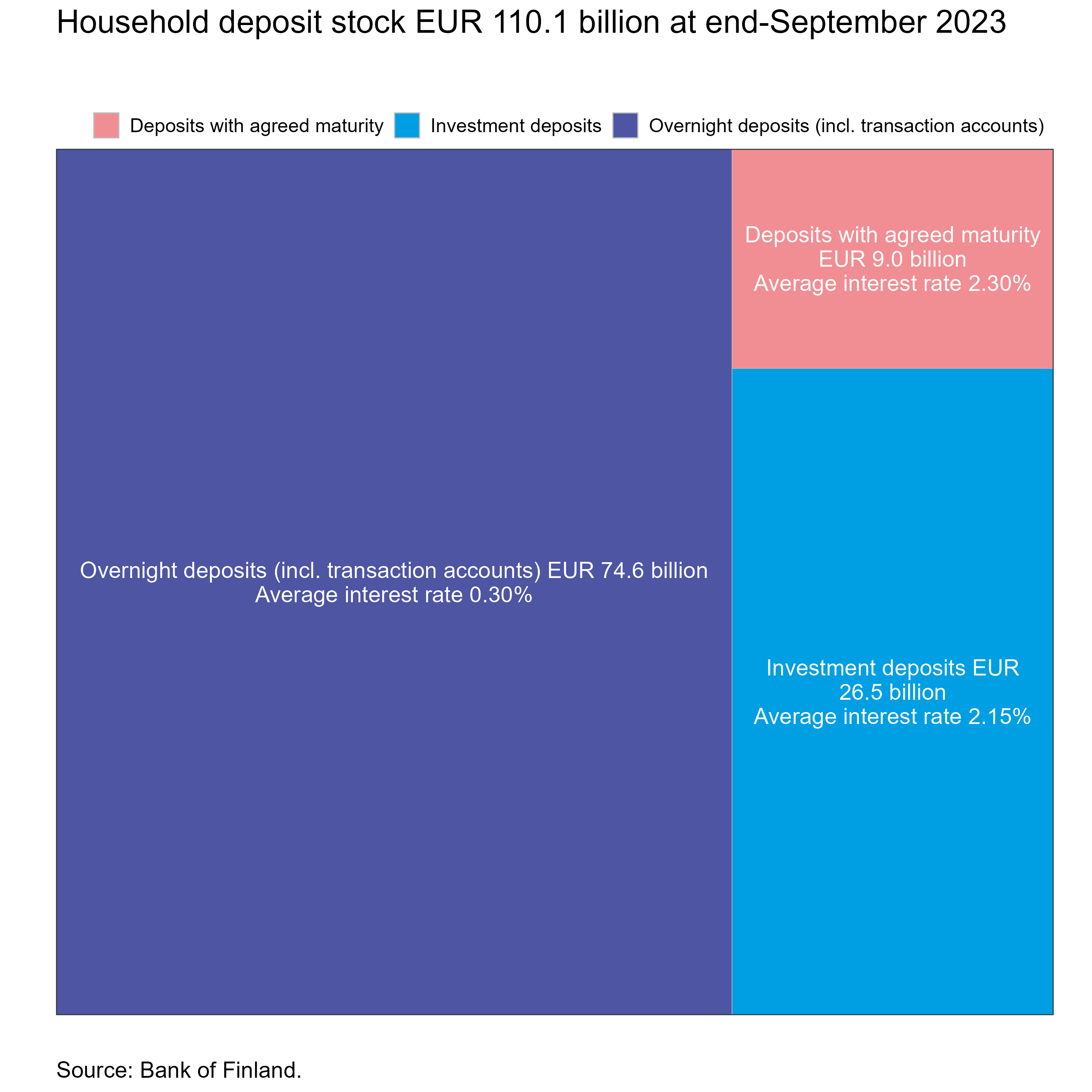

At the end of September 2023, the total stock of household deposits stood at EUR 110.1 billion. The majority of the deposits (EUR 74.6 billion) were overnight deposits, which also include transaction accounts. Most[3] of the overnight deposits (EUR 49.2 billion) were fixed-rate accounts with an average interest of 0%. Of the total deposit stock at end-September, deposits with agreed maturity accounted for EUR 9 billion, and the share of investment deposits was EUR 26.5 billion.

At the end of September 2023, the average interest rate on the household deposit stock was 0.91%, compared with 0.05% in September a year earlier. The rise in interest rates has led to a widening of interest rate differentials between the various deposit accounts. In September, the average interest rate was 0.30% for the overnight deposit stock, 2.30% for the stock of deposits with agreed maturity and 2.15% for the stock of investment deposits. The average interest rate on new agreed maturity deposits rose to 3.18% in September. New agreements made in this deposit category totalled EUR 1.2 billion, compared with EUR 240 million in September a year earlier.

In the statistics, a large amount of deposits subject to restrictive drawing provisions have been reclassified from overnight deposits to investment deposits. This has increased the amount of investment deposits and decreased the amount of overnight deposit. Historical data have been corrected from October 2022 onwards. The largest corrections in historical data pertain to October 2022 and January 2023. More details on the reclassification of deposits are available here.

Loans

Finnish households drew down new housing loans in September 2023 to a total of EUR 1.1 billion, a decline of EUR 450 million from September 2022. Of the total, investment property loans accounted for EUR 101 million. The average interest rate on new housing loans rose from August, to 4.65%. At the end of September 2023, the stock of housing loans stood at EUR 106.7 billion, and the the annual growth rate of the loan stock was -1.8%. Investment property loans accounted for EUR 8.6 billion of the housing loan stock. At the end of September 2023, Finnish households’ loan stock comprised EUR 17.1 billion in consumer credit and EUR 17.8 billion in other loans.

Finnish non-financial corporations drew down new loans[4] in September in the amount of EUR 1.8 billion, of which EUR 360 million was to housing corporations. The average interest rate on new corporate loans fell from August, to 5.45%. At the end of September, the stock of loans to Finnish non-financial corporations stood at EUR 106.1 billion, of which loans to housing corporations accounted for EUR 43.6 billion.

| Loans and deposits to Finland, preliminary data* | |||||

| July, EUR million | August, EUR million | September, EUR million | September, 12-month change1, % | Average interest rate, % | |

| Loans to households, stock | 141,675 | 141,676 | 141,596 | -1.4 | 4.41 |

| - of which housing loans | 106,855 | 106,749 | 106,719 | -1.8 | 3.86 |

| - of which buy-to-let mortgages | 8,622 | 8,640 | 8,650 | 4.05 | |

| Loans to non-financial corporations2, stock | 105,263 | 105,407 | 106,10 | 0.4 | 4.57 |

| Deposits by households, stock | 109,878 | 109,278 | 110,110 | -3.0 | 0.91 |

| Households' new drawdowns of housing loans | 1,005 | 1,139 | 1,131 | 4.65 | |

| - of which buy-to-let mortgages | 86 | 112 | 101 | 4.79 | |

* Includes loans and deposits in all currencies to residents in Finland. The statistical releases of the Bank of Finland up to January 2021, as well as those of the ECB, present loans and deposits in euro to euro area residents and also include non-profit institutions serving households. For these reasons, the figures in this table differ from those in the aforementioned releases.

1 Rate of change has been calculated from monthly differences in levels adjusted for classification and other revaluation changes.

2 Non-financial corporations also include housing corporations.

- Euro-denominated deposits and loans of euro area residents: stock, 12 month rate of change and average interest rate

- Euro-denominated loans and deposits of Finnish households

- New business on loans and new drawdowns of household loans

- Finnish contribution to the euro area monetary aggregates and their main counterparts

- Imputed interest rate margins on loans from MFIs

For further information, please contact:

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi

Antti Hirvonen, tel. +358 9 183 2121, email: antti.hirvonen(at)bof.fi

The next news release on money and banking statistics will be published at 10:00 on 30 November 2023.

Related statistical data and graphs are also available on the Bank of Finland website at https://www.suomenpankki.fi/en/statistics2/.

[1] Investment deposits are deposits redeemable at notice. They do not have an agreed maturity (unlike deposits with agreed maturity), but have a period of notice during which they cannot be converted into currency without incurring a penalty (unlike overnight deposits). This category also includes investment accounts which do not have a period of notice or agreed maturity, but which contain restrictive drawing provisions.

[2] Includes transaction accounts and other accounts from which funds may be drawn or transferred freely.

[3] Fixed-rate transferable overnight deposits.

[4] Excl. overdrafts and credit card credit.