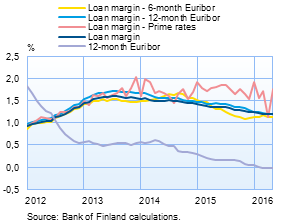

Drawdowns of housing loans picked up further in May 2016 as households drew down new housing loans totalling EUR 1.8 bn. The average interest rate on new housing loans was 1.21% with the margin accounting for 1.19%. Hence, the reference rate only accounts for a minor proportion of the total interest rate, but the statistics show that the choice of reference rate may have an impact on the margin on a housing loan. |

|

Loans New drawdowns of loans to non-financial corporations (excl. overdrafts and credit card credit) amounted to EUR 1.7 bn in May. The average interest rate on new corporate-loan drawdowns rose from April, to 1.84%. At the end of May, the stock of euro-denominated loans to non-financial corporations was EUR 73.7 bn, of which loans to housing corporations accounted for EUR 24.2 bn. |

Deposits At end-May, the stock of household deposits totalled EUR 83.2 bn, and the average interest rate on the deposits was 0.24%. Overnight deposits accounted for EUR 58.5 bn and deposits with agreed maturity for EUR 10.3 bn of the total deposit stock. In May, households concluded EUR 0.5 bn of new agreements on deposits with agreed maturity, at an average interest rate of 0.62% Notes: |

Key figures of Finnish MFIs' loans and deposits, preliminary data

| March, EUR million | April, EUR million | May, EUR million | May, 12-month change1, % | Average interest rate, % | |

| Loans to households2, stock | 122,319 | 122,718 | 123,009 | 2,8 | 1,63 |

| - of which housing loans | 92,162 | 92,471 | 92,707 | 2,6 | 1,15 |

| Loans to non-financial corporations2, stock | 73,281 | 73,551 | 73,665 | 4,3 | 1,55 |

| Deposits by households2, stock | 81,933 | 83,664 | 83,241 | 1,3 | 0,24 |

| Households' new drawdowns of housing loans | 1,402 | 1,608 | 1,748 | 1,21 |

1 Rate of change has been calculated from monthly differences in levels adjusted for classification and other revaluation changes.

2 Households also include non-profit institutions serving households; non-financial corporations also include housing corporations.

- Euro-denominated deposits and loans of euro area residents: stock, 12 month rate of change and average interest rate

- Euro-denominated loans and deposits of Finnish households

- New business on loans and new drawdowns of household loans

- Finnish contribution to the euro area monetary aggregates and their main counterparts

For further information, please contact:

Johanna Honkanen, tel. +358 10 831 2992, email: johanna.honkanen(at)bof.fi,

Olli Tuomikoski, tel. +358 10 831 2146, email: olli.tuomikoski(at)bof.fi

The next news release will be published at 1 pm on 29 July 2016.

http://www.suomenpankki.fi/link/2331b6266da3492f832ec75e0f654bd9.aspx?epslanguage=en.